The article was written on and first appeared on taxpolicycenter.org

Both Hillary Clinton and Donald Trump have proposed income* tax changes that would result in less charitable giving. While the effects are indirect, the Tax Policy Center estimates that Trump’s plan would reduce individual giving by 4.5 percent to 9 percent, or between $13.5 billion and $26.1 billion in 2017, while Clinton’s plan would reduce giving by between 2 percent and 4 percent, or $6 billion to $11.7 billion.

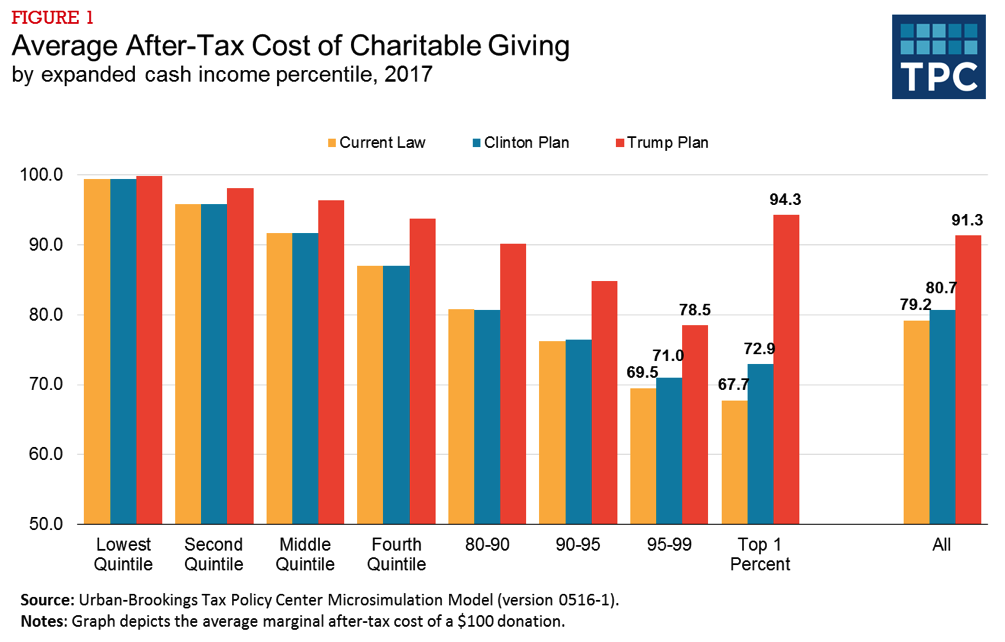

The actual reduction in charitable gifts would depend mainly upon how responsive givers would be to smaller tax incentives. However, higher-income taxpayers would be affected the most. Lower-income households would not likely reduce giving since most do not itemize deductions today and would not under either the Trump or Clinton plans.

Figure 1 summarizes the increase in the cost (reduction in incentive) of giving under the two plans. The Clinton plan only affects the cost of giving for those in the top 5 percent, while Trump’s plan raises the cost of giving for those at all income levels.

Start with Trump, who would reduce the tax benefits of charitable giving in three ways:

First, by reducing marginal tax rates he’d increase the after-tax cost of charitable giving. If you give away $100, you don’t pay tax on that $100 of income, so the after-tax cost of the donation for someone in today’s 39.6 percent top tax bracket is only about $60—the $100 gift minus $39.60 in tax savings. But by reducing the top rate to 33 percent, Trump would raise the after-tax cost of that $100 gift to $67.

Second, by raising the standard deduction to $15,000 ($30,000 for couples), Trump would sharply reduce the number of taxpayers who itemize. People who stop itemizing can no longer deduct their charitable contributions and thus lose the tax break. In 2017, 27 million of the 45 million who now itemize would opt for the standard deduction, a decline of 60 percent.

Finally, Trump would cap itemized deductions at $100,000 for singles and $200,000 for joint filers. IRS data indicate that in 2014 taxpayers with over $1 million in adjusted gross income (AGI) deducted an average of $165,000 for charitable contributions and another $260,000 for state and local taxes. Since the state and local tax deduction alone would exceed Trump’s proposed cap on itemized deduction, many high-income taxpayers would lose their tax incentive to give to charity.

While all these changes might discourage charitable giving, Trump’s generous tax cuts would also leave taxpayers more money to give to charity. This would particularly be true for very high income households: In 2017, tax cuts for people in the top 1 percent would average more than $200,000.

Clinton’s plan would do little to change the giving incentives of taxpayers for the bottom 95 percent of the income distribution. She’d slightly increase incentives for low- and middle-income taxpayers to give to charity by boosting their after-tax incomes.

In contrast to Trump, Clinton would significantly raise taxes on high-income households. She’d impose a 4 percent surcharge on adjusted gross income (AGI) in excess of $5 million, increase capital gains rates based on holding periods, create a minimum tax of 30 percent of AGI phasing in between $1 and $2 million of incomes, and put a 28 percent limit on the value of tax benefits from deductions other than the charitable deduction. On net these not only decrease after-tax incomes, but also lead some current itemizers to take the standard deduction and thereby lose the charitable deduction. The proposal with the largest effective on giving incentives is the 30 percent minimum tax (i.e., the “Buffett Rule”), which would reduce the incentive for affected taxpayers.

Overall both candidates would reduce the tax incentives for giving to charity, probably not what either really intended.

*This analysis only includes changes in the federal income tax. Both Clinton and Trump have also proposed significant changes to the estate tax that would impact incentives to donate to charity and leave charitable bequests. Clinton’s proposal to lower the estate tax threshold and increase estate tax rates would increase giving incentives, while Trump’s proposal to eliminate the estate tax would reduce them.

http://www.taxpolicycenter.org/taxvox/both-clinton-and-trump-would-reduce-tax-incentives-charitable-giving